QI TAKEAWAY — “Transitory” inflation is now catalyzing bankruptcies in America. As much as we hear about the bravado of job hoppers, job losses necessarily follow companies going out of business. The ‘stag’ in stagflation is rearing its ugly head. We know we’ve been swimming upstream for months against the tide of buyside and sell-side steepening calls. We remain comfortable with our call.

- Bankruptcy filings for companies with at least $50 million in debt hit three in the week ended November 12 vs. nearly 15 seen in June 2020; though the Fed’s credit backstop limited creative destruction, corroded supply chains are pressuring firms that survived the pandemic

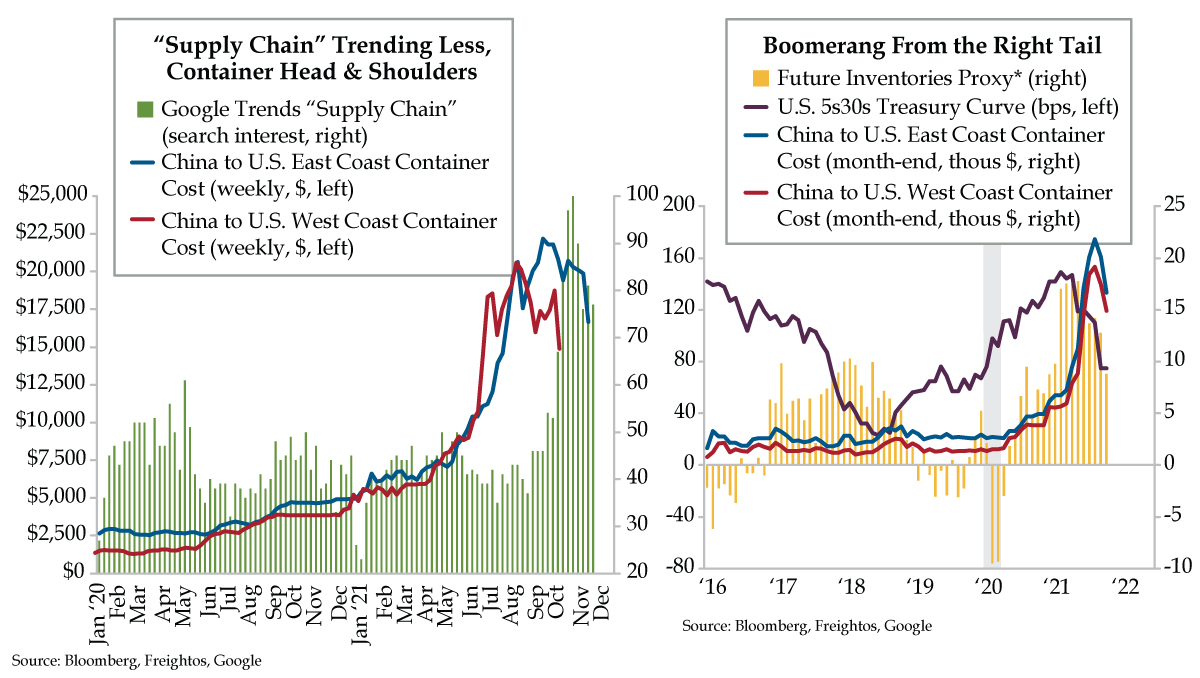

- An average of Future Inventories from regional Fed surveys suggests that panic buying by firms has subsided; the same message, which harms future GDP math, can be seen in the tightening of the 5s/30s curve corroborated by a decline in Google “Supply Chain” searches

- Per Freightos, container costs from China to the US’s East and West Coasts have finally begun to turn; should the downward trend continue, prices may begin to fall back down to Earth for consumers as well as for businesses struggling to manage elevated input costs

The Feather — Charts of the Week

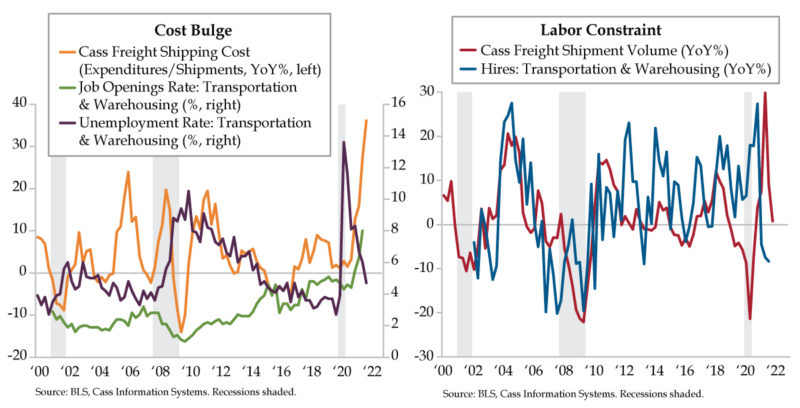

A Labor of Locks

VIPs Bankruptcy filings for companies with at least $50 million in debt hit three in the week ended November 12 vs. nearly 15 seen in June 2020; though the Fed’s credit backstop limited creative destruction, corroded supply chains are pressuring firms that survived the pandemic An average of Future Inventories from regional Fed surveys suggests […]

Danger, Will Robinson!

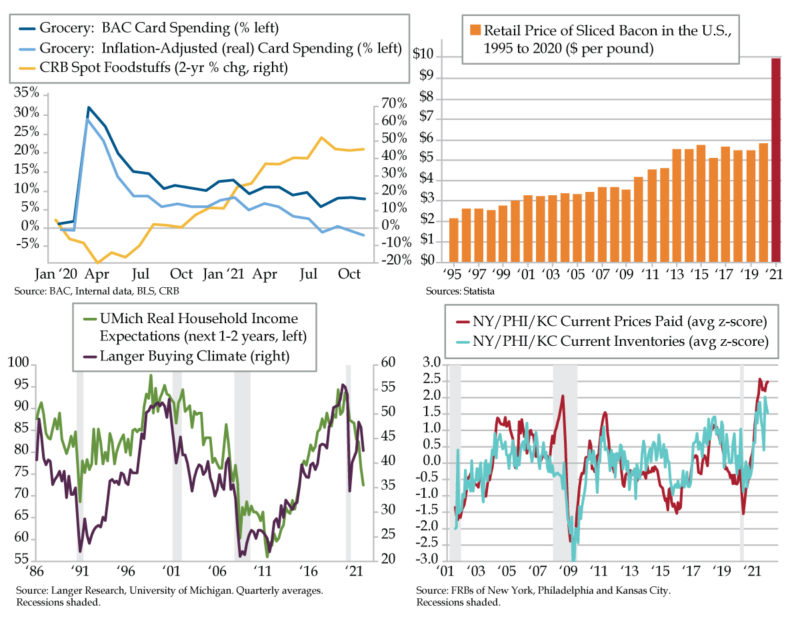

VIPs Per Bank of America, the percentage change in inflation-adjusted grocery spending on a 2-year basis slipped further into contraction in October; while food inflation appears to be leveling off at high levels, per the CRB, higher prices are driving nominal gains in card spend On an inflation-adjusted basis, growth in goods spending reached a […]

Hysteron Proteron Club

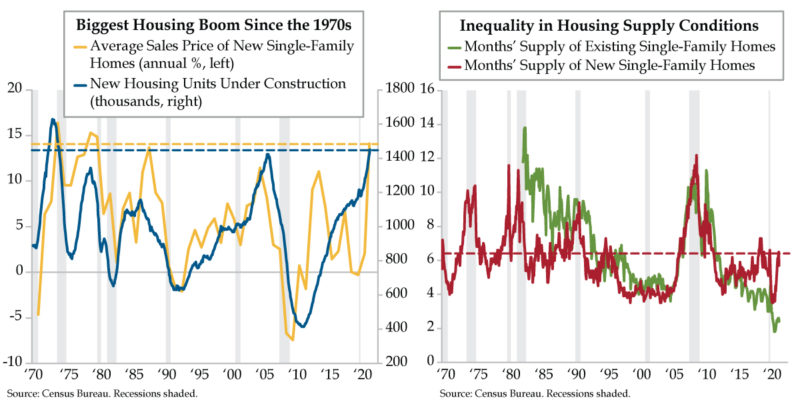

VIPs New homes under construction rose to 1.451 million in October, eclipsing the 2000s peatilk of 1.426 million circa March 2006; the last time units under construction were higher was the 1970s, though the current boom critically lacks the same underlying population growth rates Unsold existing single-family home inventories sit at 2.4-months, a record […]

King of the Catch Phrase

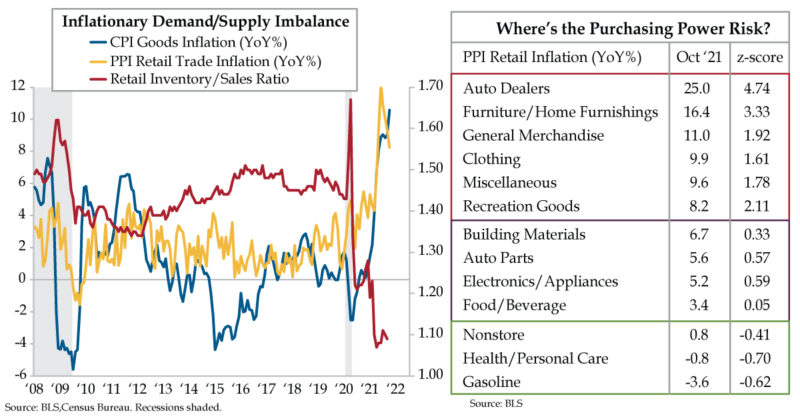

VIPs October’s 1.7% MoM retail sales print was the largest since March and more than four times greater than the 0.4% long-term average; however, given these are nominal terms, deflating them using the CPI shows real retail sales remain 6% below March’s post-pandemic high At 1.09, September’s retail inventory/sales ratio hovered just above April 2021’s […]

Not Archimedes Principle

VIPs Cass freight shipping costs saw a 36.2% YoY gain in October, the largest on record, as supply chain disruptions persist; though logistics costs have surged, shipment volume has calmed thus far in Q4 to a 0.8% YoY advance vs. the 29.9% and 9.1% gains of Q2 and Q3 The American Trucking Association estimates […]